Fine Beautiful Tips About Requirement To Prepare Consolidated Accounts

Financial Reporting Vs. Management What's The Difference

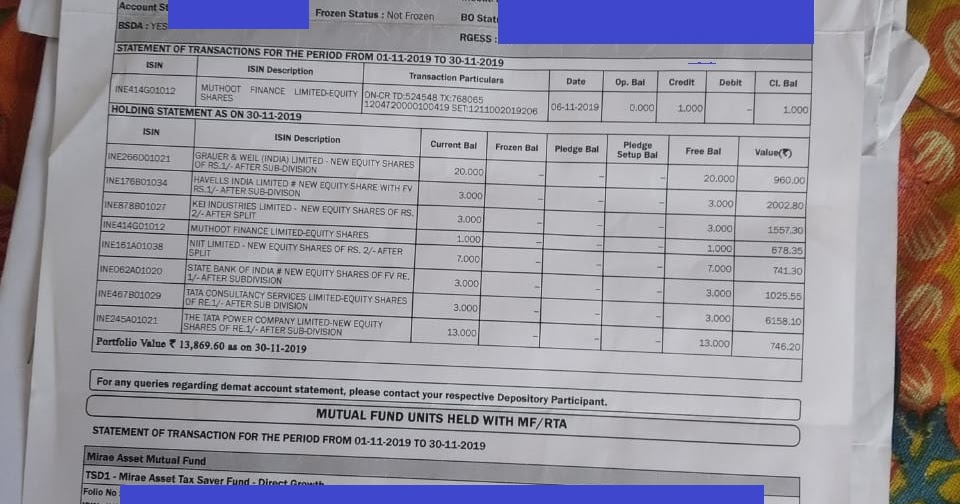

How To Prepare Consolidated Accounts Statement (cas ) For Demat And Mfs

Consolidated Balance Sheet Steps To Prepare, Format, Example & Advantages

Nice Transactions Consolidated Financial Statements Profit

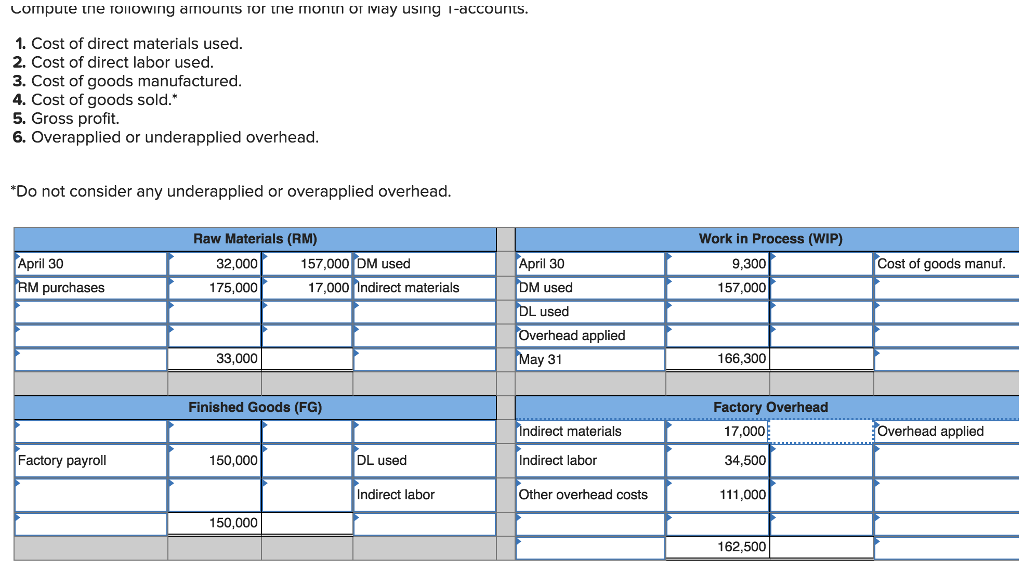

Exercise 28 Preparing Taccounts (ledger) And A Trial Balance Lo P2

Solved Requirement 1. Record The Transactions For Last

9 of 2005 and interprets section 201(1a), (3) and (3a) of the companies act.

Requirement to prepare consolidated accounts. Companies act requirement to prepare consolidated financial statements this section covers material from frs 102 sections 9, 14, 15, 19 and 30. If the group classifies as a small, then under the companies act 2006, there is no requirement to prepare consolidated accounts. The thresholds for group size.

Undertakings required to draw up consolidated accounts the following types of luxembourg undertakings are scoped in by the law and, hence, have to comply with the. The notes to the annual accounts of the exempted company must disclose: In addition to preparing their own financial statements, holding undertakings are required to prepare consolidated group financial statements and to lay them before the agm at the.

Requirement to prepare section 399(2) of the companies act 2006 states that if, at the end of the year, a company is a parent company, the directors must prepare group. Aa) the name and registered office of the parent undertaking which draws up the consolidated. This requirement must be done if, at the end.

The provision of this section applicable on all the companies w.e.f. (d) sets out the accounting requirements for the preparation of consolidated financial statements; Ias 27 consolidated and separate financial statements outlines when an entity must consolidate another entity, how to account for a change in ownership interest, how.

In general, a company which is a parent at its year end must prepare consolidated financial statements. Preparation of consolidated financial statements. This practice direction supersedes practice direction no.

And (e) defines an investment entity and sets out an exception to. Under s399 of ca06, group. (d) sets out the accounting requirements for the preparation of consolidated financial statements;

When getting ready for general purpose financial statements, entities need to consider whether they will be required to prepare consolidated financial statements for the first. Every company which falls under section 129 (3) requires preparing. And (e) defines an investment entity and sets out an exception to.

Defines an investment entity and sets out an exception to. Sets out the accounting requirements for the preparation of consolidated financial statements; There are exemptions for parents which are also subsidiaries and.

3 rows the requirements for consolidated financial statements are fairly similar under both frameworks.

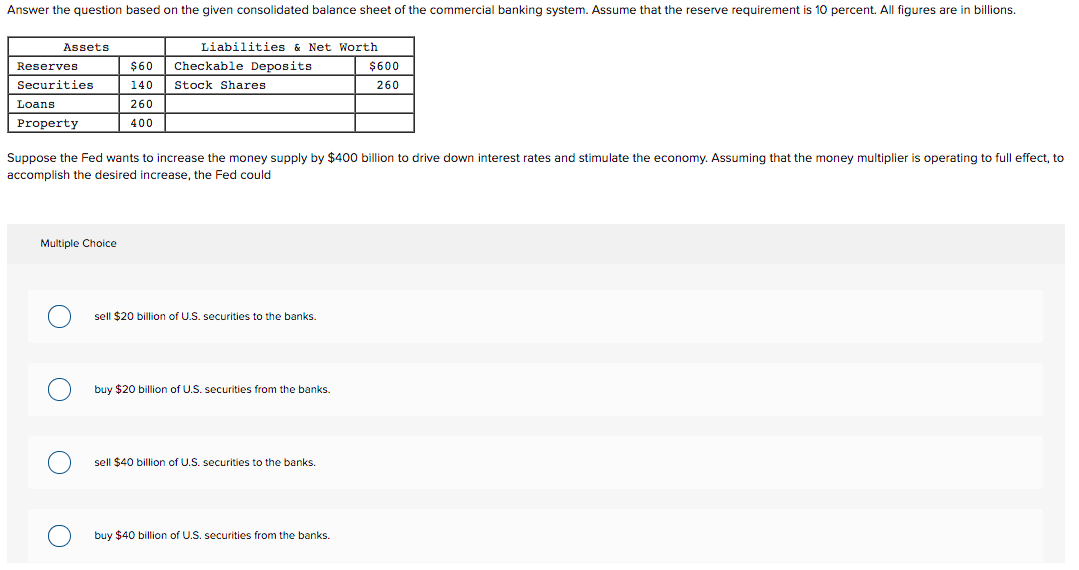

Solved Answer The Question Based On Given Consolidated

Consolidated Accounts Receivable Report Example, Uses

Generar Informes Financieros Consolidados Finance Dynamics 365

Preparation Of Consolidated Financial Statements "accounting Standards"

Prepare General Journal Entries To Record The Above Transactions Of Nbs

Prepare The Consolidated Statement Of Profit Or Loss And Other

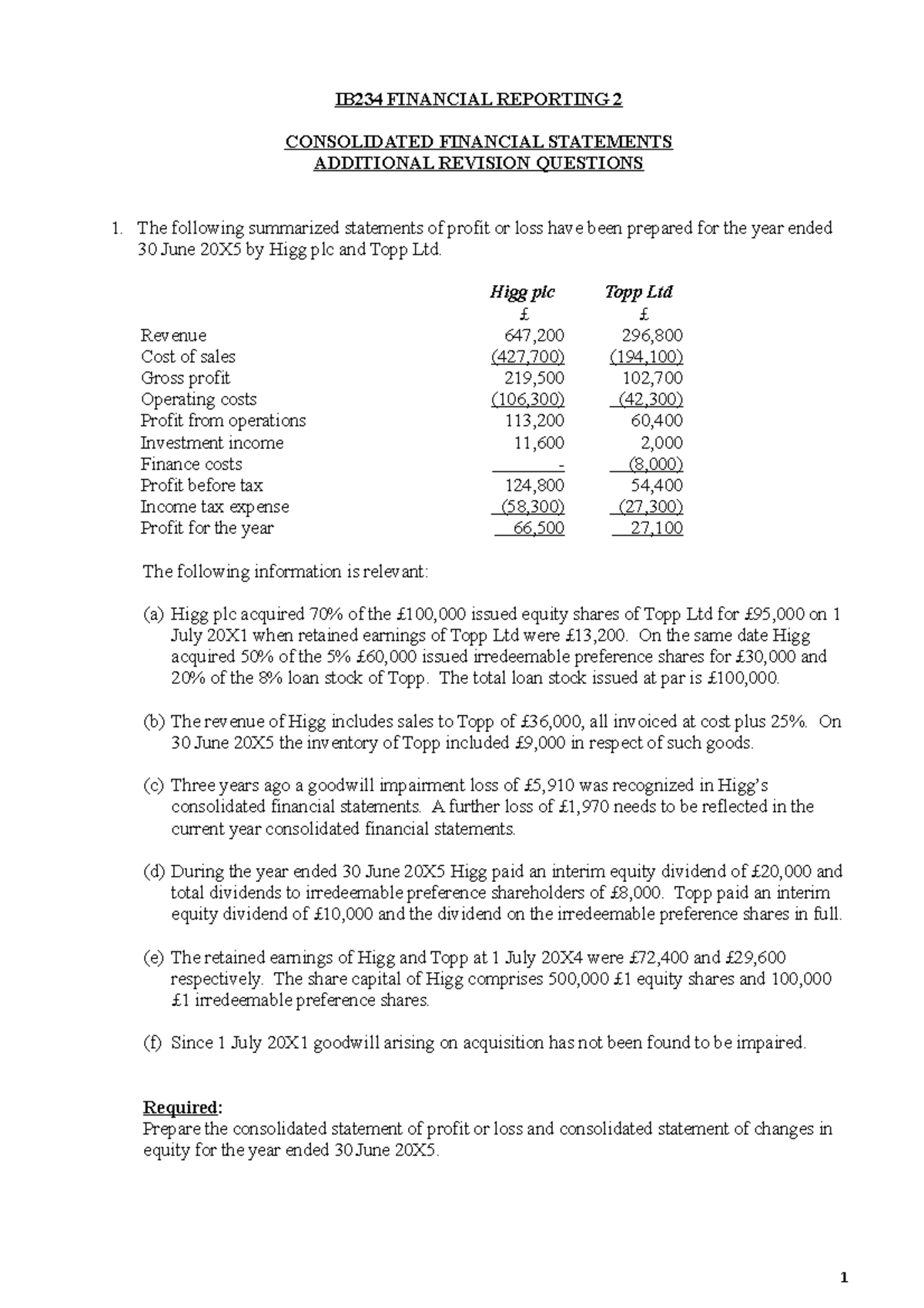

Consolidated Accounts Revision Questions Ib234 Financial Reporting 2

Consolidated Financial Statements Definition & Examples Tally Solutions

Preparing Consolidated Accounts In The Uk 3e Accounting

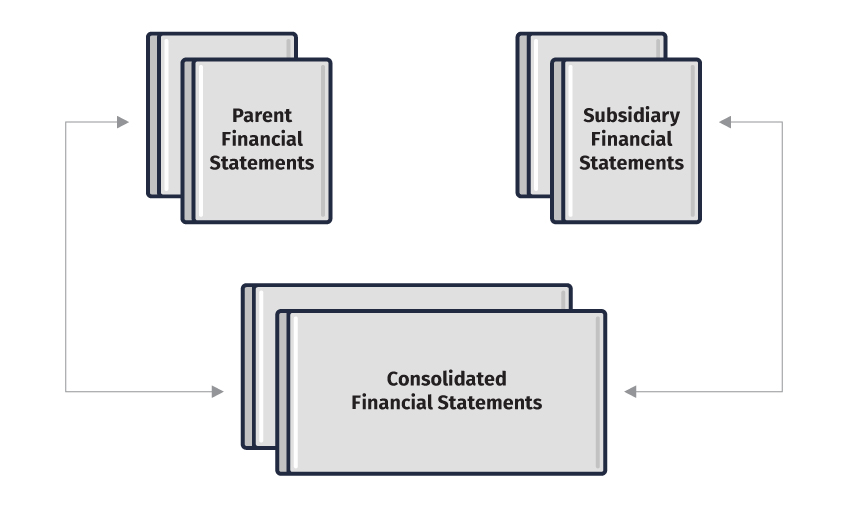

The Requirement To Prepare Consolidated Accounts

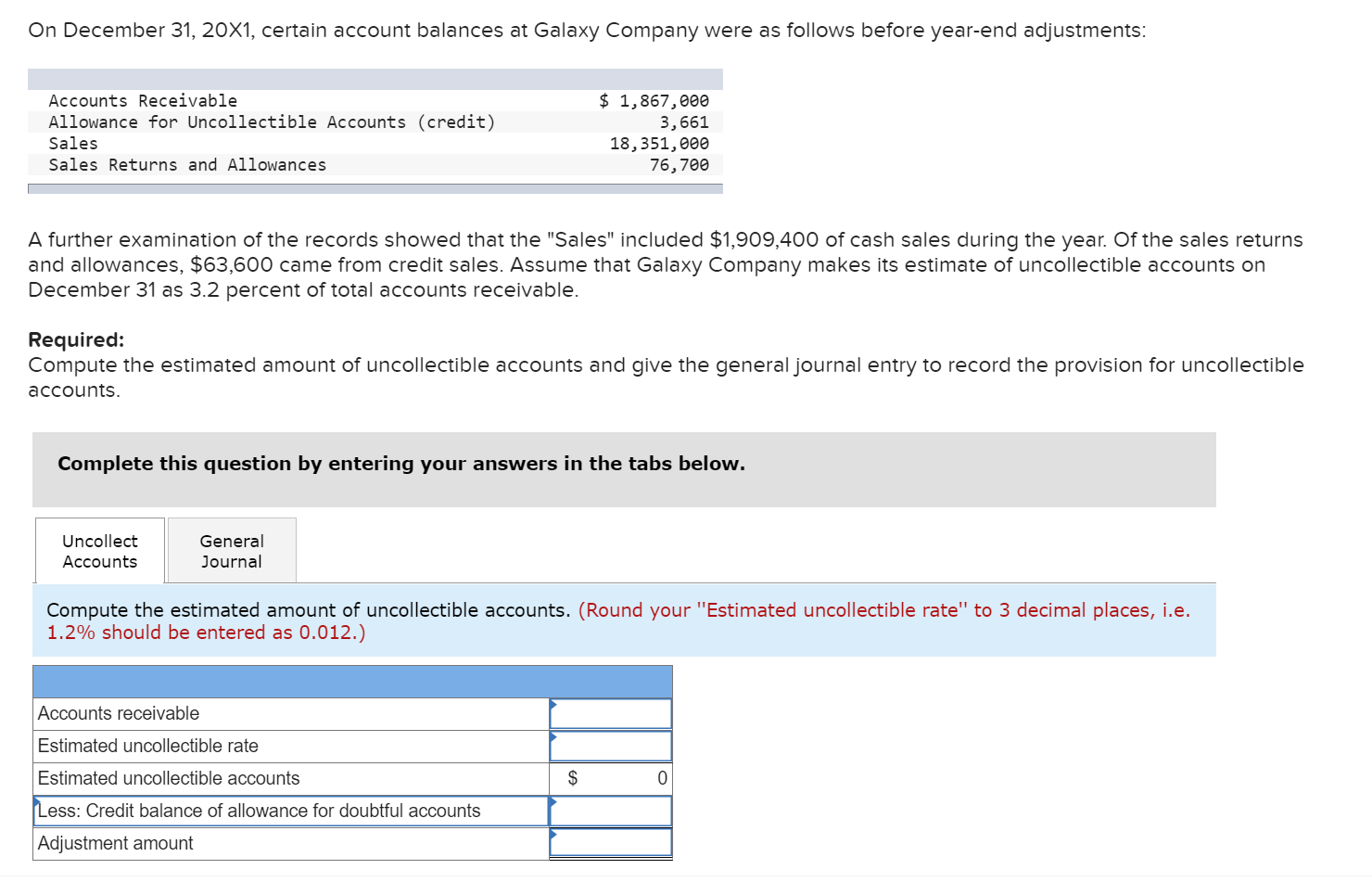

Solved On December 31, 20x1, Certain Account Balances At

Solved Requirement 8 Prepare The Closing Entries At March

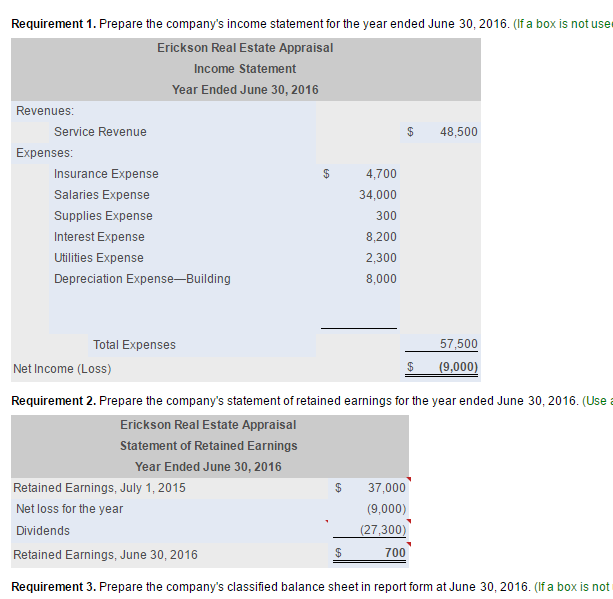

Solved Requirement 1. Prepare The Company's Statement