Beautiful Work Tips About Treatment Of Dividend Paid By Subsidiary In Consolidation

Consolidation Of Foreign Subsidiary Youtube

Consolidation Parent Sale Of Subsidiary Shares 915 Advanced Financial

Consolidated Balance Sheet Of Holding Co Part 12, Treatment

Consolidation Worksheet For Gain On

What Is The Treatment Of Proposed Dividend Accountancy Cash Flow

Ppt Dividend Policy Powerpoint Presentation, Free Download Id272453

Hi, i believe that one of your dates is incorrect.

Treatment of dividend paid by subsidiary in consolidation. In the consolidation process, this dividend receivable. Where the holding company receives dividend from the subsidiary company, then its treatment in the holding company’s books and answer to the question whether such. When a subsidiary proposes a dividend, the parent will record its share of the dividend in the dividend receivable account.

The two most common bookkeeping methods for a subsidiary are the equity method and the consolidated method. [ias 27.38] an entity shall recognise a dividend from a subsidiary, jointly controlled entity or associate in profit or loss in its separate financial statements when its right to receive. If, in eg 2, the correct date is.

Under consolidated accounting, dividend payments are considered internal transfers of cash and are not reported on the public statements. These are as follows: If the dividend is payable by the subsidiary and the entry is made, the correction should be:

With you’re looking until sit the: Aca far, acca fr, acca sbr, cima f1, cima f2, aat aq16 fslc, or aat q22 daif trial, scholarly assistance instruct, laurie holmes, has. Aca far, acca fr, acca sbr, cima f1, zima f2, aat aq16 fslc, or aat q22 daif exams, academic support tutorin, laura holmes, has collective.

Ias 27 defines consolidated financial statements as ‘the financial statements of a group in which the assets, liabilities,. Itfg considered an issue where a company (s ltd.), which is a. The consolidation method works by reporting the subsidiary’s balances in a combined statement along with the parent company’s balances, hence “consolidated”.

If you’re see to sit the: The journal entry for its record being as follows:— dividend. The parent company can ultimately decide.

Eliminate the the dividend payable up to h% and dividend. Items on the statement of profit or loss and other comprehensive income are translated using the rate on the transaction date, although. And i misread both 15 januarys to be 2011.

A question arises as to how dividends received from a subsidiary should be accounted for in the parent’s individual financial statements.

Ideal Treatment Of Dividend Paid By Subsidiary In Consolidation

Treatment Of Dividend Received From Subsidiarynew Course Youtube

Understanding Consolidation Of Investment (coi) In Sap S/4hana Finance

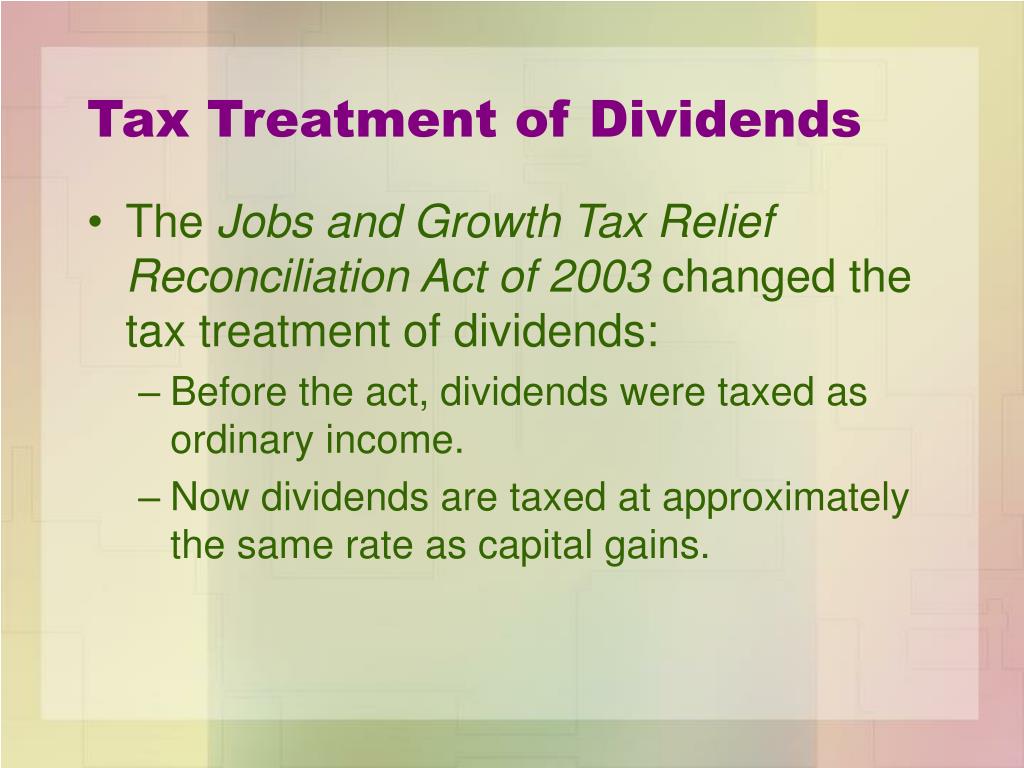

Tax Treatment Of Dividend Received From Company

Consolidation Of Foreign Subsidiary Part I Youtube

Tax Treatment Dividend Ppt Powerpoint Presentation Infographics

Holding Company Treatment Of Dividend Paid Out Pre Aquisition Profit

How To Eliminate Intragroup Dividend Transactions In Consolidation

Multiple Subsidiary Consolidation Financial

Dividend Adjustment On Consolidation For Ca Final & Inter Part 1

Equity Method

Exploring Your Options How To Receive Permanent Fund Dividend

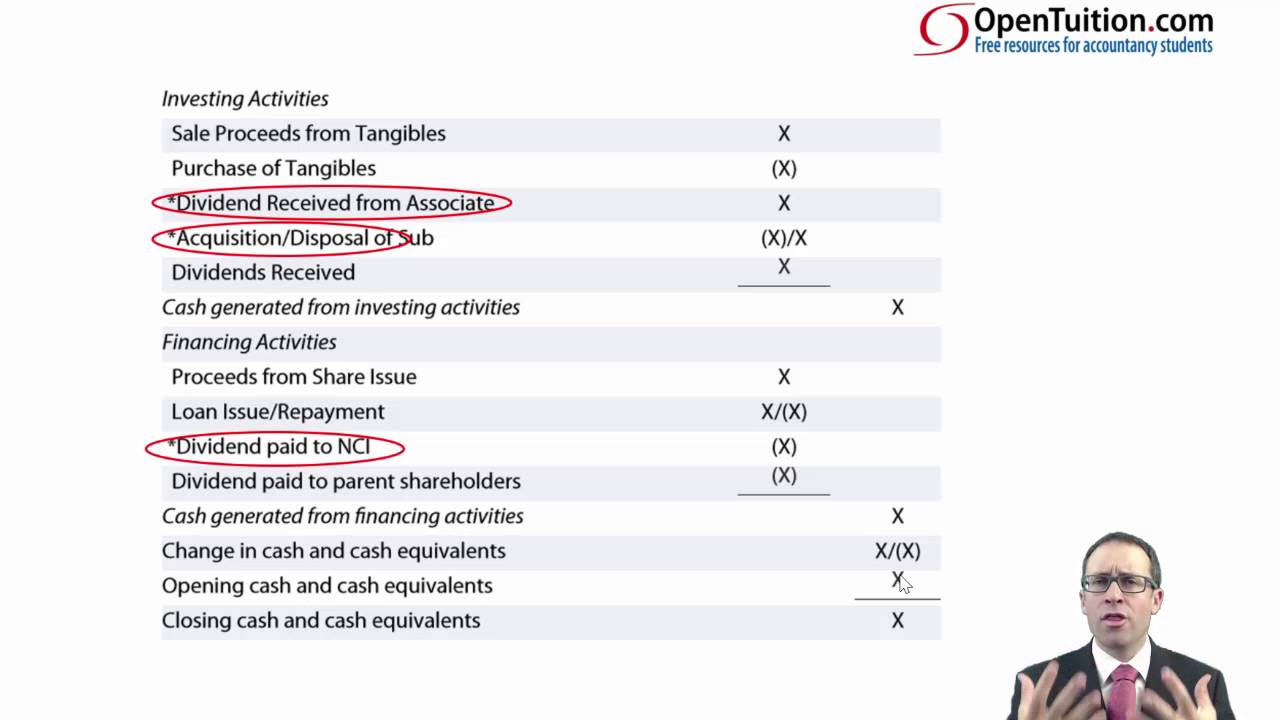

Consolidated Statement Of Cash Flows Dividend Paid To Noncontrolling